/CMS-LI-savings-header_q4coeq.jpg)

Before deciding on a policy, you should first understand life insurance. A life insurance policy offers a contract between you and your insurance company to provide a death benefit to your beneficiaries if you pass away during the term of the policy.

Your beneficiaries are the loved ones or entities you select to receive a monetary payout, also known as a death benefit, if you die while the policy is active.

There are two main types of life insurance:

- Whole life insurance: This type of insurance doesn't expire and covers you for your entire life as long as you keep up with your premium payments. Whole life offers a fixed premium and typically includes a savings element in addition to the death benefit.

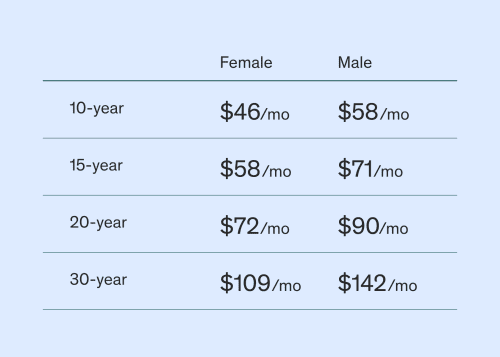

- Term life insurance: You get coverage for a specific period that you select, usually when you need it most. At Ethos, we offer term life insurance coverage from $20,000 to $2 million, and our term lengths range from 10 to 30 years. Once your policy ends, you may be able to renew the policy.

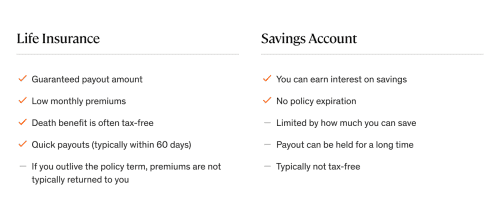

Having a robust savings account can give you a sense of financial security. But what if the unexpected were to happen and you were to pass away suddenly? Suppose your significant other is suddenly faced with a mortgage, your outstanding debt, and college tuition for your children—without your income? That's where a life insurance policy can help provide peace of mind for you and your loved ones. You get to control the payout amount and term length, and you can rest easy knowing the payout will come quickly when your loved ones need it most.

A savings account could get depleted quickly

The sad reality is that a funeral may be the first financial order of business your loved ones will face if you pass away. Consider that the average cost of a funeral in the United States runs close to $8,000. Now take into account that more than 50% of Americans say they have less than $3,000 in their bank accounts. Add in the average household credit card debt of over $5,000, and it's clear to see the importance of having a life insurance policy to help protect your family and cover lost wages, mortgage payments, and day-to-day expenses.

Understanding the cash value of life insurance

As you become more familiar with different types of online life insurance, you'll find that specific whole life insurance policies may have a cash value component that lets you earn interest. Some policies will let you withdraw or borrow against it if you need to.

What if I outlive my term policy?

Your term life insurance policy is important to consider during your more significant earning years. Once you've established other funds and paid off any debt, your savings becomes an important source of funds when you hit retirement. Having both life insurance and a savings plan in place shouldn't be an either-or decision. By setting your family up for financial security after your income-earning years through savings, your life insurance policy no longer becomes your single source of financial safety.

Term life insurance offers some of the more affordable life insurance available. The monthly premium you'll pay may vary based on factors such as your age, gender, family history, health, smoking status, occupation, and hobbies. Your policy remains active as long as you pay your premiums. If you pass away, your beneficiaries receive a guaranteed lump-sum amount that's typically tax-free and paid within 30 to 60 days.

Life insurance is an important financial move you can make today to help protect your family tomorrow. Our easy online tools make it quick and straightforward. Gone are the days of drawn-out paperwork, visits, and medical exams. With the power of modern predictive analytics and technology, Ethos has crafted a seamless online process.

With Ethos, you can determine the plan that suits you best at a premium rate you can afford in just minutes.

/Stocksy_txpd617015cclW200_Medium_2772165_fq8edr.jpg)

/Stocksy_txpd2ae323dqYV200_Medium_2347940_y1y3u1.jpg)