Life Insurance for Women: Our Guide

/_Life_insurance_for_women_f2yebk.jpg)

Women account for more financial security in a family than ever before. According to the US Bureau of Labor Statistics, approximately 57% of women are in the workforce, and nearly 55% of married couples function as dual-income households. Additionally, women are increasingly the primary breadwinners for their families.

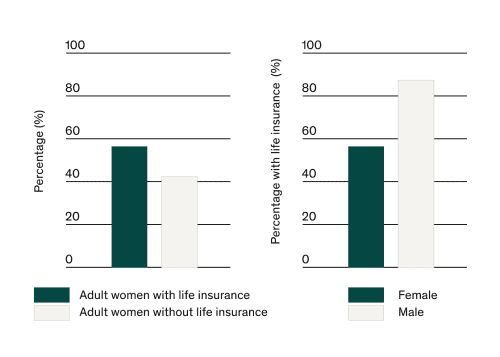

When it comes to carrying a life insurance policy, women often lag behind men. Research from the Life Insurance Marketing and Research Association (LIMRA) found that only 47% of women in the U.S. have active life insurance policies. And of the women that do, their policies typically provide much less coverage than men's, despite having the same needs.

Life insurance protects your loved ones. The people you name in your life insurance policy (your beneficiaries) receive the financial death benefit if you pass away while your life insurance policy is active. That's reason enough for women to search their life insurance options.

Women are significant drivers for household income and finances and often have key responsibilities in the home, traditionally serving as primary caregivers for their children and parents. For single mothers, all responsibilities fall upon their shoulders.

It's a lot of work, but the value of that work is often overlooked. That's especially true in households with a stay-at-home mother. While full-time moms may not be contributing an income from an outside place of work, the value of their work is significant. For many women, that gap in life insurance coverage can significantly impact the family left behind.

/20Q2-CMS003-02-life-insurance-case-for-coverage_2x_ovjhra.png)

Term length

When considering how long you'll need coverage, the key is to think long-term. Depending on your situation, you may need to replace your income or equivalent childcare costs, pay for debts, and cover funeral costs — or some combination of several expenses.

You'll need to ensure you're covered for as long as you expect to carry those responsibilities. For example, a stay-at-home mom with kids entering college may only need a 10-year policy, while a young single woman at the start of her career may opt to lock in a 30-year policy, so she's prepared for the future. Even if you're a stay-at-home mom, a single mother, or the primary breadwinner for your household of one, it's critical to protect your loved ones. Life insurance can help.

Coverage amount

Calculating coverage can seem tricky, but you just need enough coverage to ensure your loved ones won't have to worry about additional expenses, such as your shared mortgage, car payments, or childcare. It can help to think about it in terms of how much income you'd bring in over the term length you select, in addition to any debt you'd accrue over that same time.

A straightforward way to understand coverage amounts features the DIME formula (debt + income + mortgage + education), adding together each of the four areas to determine your coverage amount needs. In this formula, add total debts, your current income multiplied by the number of years you estimate your family would need it, the amount left on your mortgage, and an estimated cost of sending your kids to school.

Women must understand how important life insurance is for them. Even if you are a stay-at-home mom, a single mother, or the primary breadwinner for your household of one, it's critical to protect your loved ones. Life insurance can help.

Even if you get life insurance through your employer, it's often not enough for the coverage you may need. Your employer-sponsored plan may be worth 1-2X your annual salary. However, experts recommend coverage levels of approximately 10X your current salary. It's also important to consider that your employer-sponsored life insurance plan may not travel with you if you change jobs or are unemployed (find more information about life insurance if you're unemployed).

Having a term life policy of your own can ensure you're covered regardless of your job situation, so that your loved ones remain financially protected.

As a stay-at-home spouse, you provide a serious benefit to your family — one that would have to be paid for if you were no longer there. Your surviving spouse would need to cover costs related to childcare and home management, which can certainly add up. Just because stay-at-home moms don't bring in outside income doesn't mean life insurance isn't necessary.

Single moms carry the sole responsibility of providing for and taking care of their families. That means it's critical to have life insurance, especially with young, dependent children.

A term life insurance policy can help give you peace of mind. If something were to happen, your children would have financial security.

Many women live in the so-called "sandwich generation," caring for both children and older parents or relatives. You may be shouldering the burden of healthcare costs for your parents or saving the family money by providing the services yourself. Your loss would leave a large financial hole in the entire family while disrupting the type of care your loved ones receive. Life insurance can fill the financial void.

Don't forget that life insurance benefits more than a spouse or children. At the very least, most people have debts and funeral expenses that need covering. Many single women also take on the role of caretaker for an aging parent or sibling.

And if you need to alter a policy after a divorce, Ethos can help.