Life insurance 101

/Stocksy_txp738c49e9tCW200_Medium_1196806_lnayl8.jpg)

Simply put, life insurance is a way to provide financial protection for your loved ones in their most vulnerable moments. A life insurance policy ensures that if you die while your policy is active, your loved ones will receive a lump-sum payout, known as a death benefit. The death benefit can be used to cover things like mortgage or rent payments, education costs, funeral arrangements, and more.

In its simplest state, every life insurance policy is made up of these four components:

- Insured - The person whose life is covered under the policy. Typically, this is the person who owns the policy and pays the premiums, however, it is possible for the policy owner and payor to be someone other than the insured.

- Beneficiary - The person(s), entity, or institution(s) that receive the death benefit if the insured person dies. You can name one person (or more) as beneficiaries when you purchase a policy.

- Premium - The money paid to keep a policy active. Payment ensures that the insurance company will provide your beneficiaries with the stated death benefit in the event of your passing. If you stop paying premiums, the policy lapses.

- Death benefit - The money paid out if the insured person passes away. Death benefits are generally not subject to an income tax and beneficiaries usually receive the benefit in one lump-sum payment

As long as the premiums are paid, this type of coverage is active for your whole life, guaranteeing the eventual payout of a death benefit. It can cost 5-10X more but if the premium is within budget, it can be a good option for anyone interested in insurance that accumulates cash value and doesn’t end.

- Most types of permanent life insurance offer a cash value component that accumulates as policy premiums are paid. This cash value typically grows with a guaranteed minimum rate of return.

- In most cases, the insured person can borrow against the cash value that’s accumulated in the policy, withdraw the cash value, or leave it in the policy to increase or maintain the death benefit.

- Due to the duration of the coverage and cash value accumulation possibilities, premiums for permanent coverage are typically more expensive than those for term life insurance.

Real-world example: Frank is 68 years old, and retired. He wants to make sure he doesn’t saddle his loved ones with expenses when he passes away. He’s looking for coverage that doesn’t expire, so he can guarantee the payout of a death benefit that will take care of his final expenses. A whole life policy makes the most sense for Frank because he will be covered for the duration of his life.

Term policies last for a specific amount of time (your term), and there is no cash value accumulation. The death benefit is only payable to the beneficiaries upon the death of the insured person during the term. Because it costs less and is more straightforward it's a good option for many people.

- You are able to choose the length of your term and the amount of coverage that would be paid out to your beneficiaries if you die before your term ends. If you die after your term ends, no death benefit is paid. It’s that simple.

- If you outlive your term, you will typically have the option to renew your policy.

- Term life insurance premiums usually cost less than permanent life insurance, making it an affordable option for many.

Real-world example: Sarah is a married, 35-year-old mother of 2 young children. She’s the primary breadwinner for her home, and she wants to ensure that her children will still be able to attend college in the event of her untimely death. For Sarah, a term policy makes the most sense. By structuring the term length around the time her children expect to make it through school, she can protect her children's educational future.

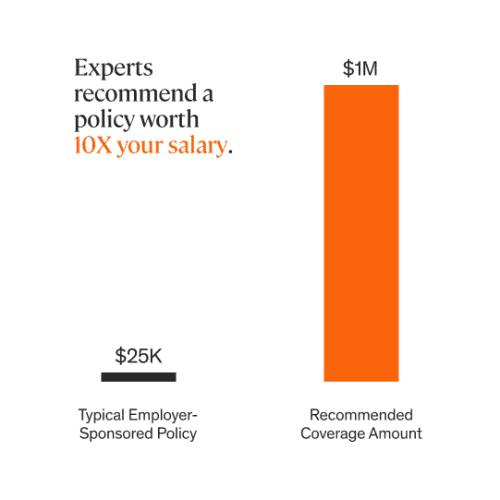

Group life insurance typically comes in the form of an employer-sponsored life insurance policy. You may already have some coverage provided to you as an employee benefit. However, this type of policy might only provide a fraction of the coverage you need. For this reason, many people buy an individual term life insurance policy to supplement the coverage they receive through work.

It ultimately depends on the personal and financial circumstances of each individual. In general, you can find your ideal coverage amount by calculating your long-term financial obligations and then subtracting your assets. The remainder is the gap that life insurance needs to fill. It can be difficult to know what to include in your calculations, so we created a life insurance calculator to help you determine your coverage needs.

/Stocksy_txpdeed79ffiNb200_Medium_1735774_njv09q.jpg)

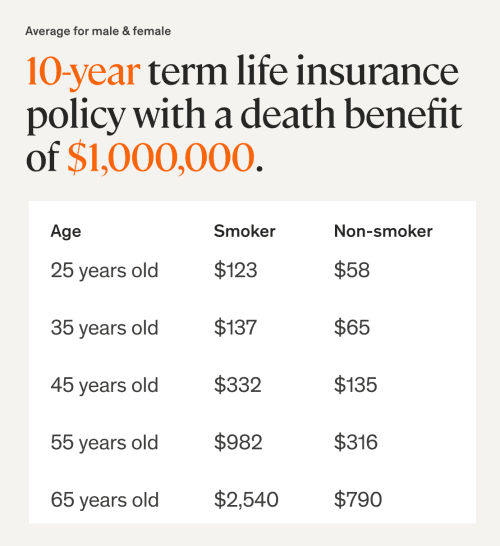

It’s different for everyone and varies based on your unique situation. The biggest factors that can affect your premium include:

- The type of policy you choose: Whole life policies tend to cost more than term life policies because they last for your entire life, and accumulate cash value.

- The type of underwriting experience you want: Simplified and guaranteed issue policies tend to be more expensive because they don’t require full underwriting and are written without a medical exam.

- Your coverage amount and term length: Less coverage and shorter term lengths tend to cost less–that’s another reason whole life policies cost more, they never expire.

- Your age: Younger people typically have lower rates.

- Your health status: Healthier people typically have lower rates.

- Your tobacco use: Non-smokers typically have lower rates.