A life insurance guide for new parents

/_Life_insurance_guide_for_new_parents_fh2gfp.jpg)

Let's cut to the chase. Kids are expensive to raise.

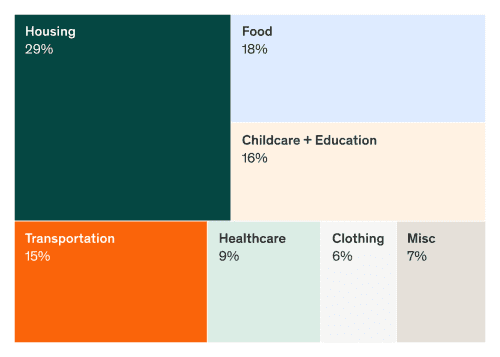

Getting your bundle of joy from the crib to college costs a lot of money. According to a study from the US Department of Agriculture (USDA), an average middle-income family can expect to spend approximately $233,000 to raise a child through the age of 17. This number includes the cost of your home or apartment, as well as daily necessities such as food and childcare. However, this doesn’t even include higher education.

Add college into the mix and your costs become higher. While your family might qualify for financial aid, it may not be enough to cover the rising costs of college.

Whether you’re already a parent or just starting a family, many financial and insurance experts recommend that you understand the cost of having a family and how life insurance can protect your loved ones in the event that you pass unexpectedly. As a guideline, make sure you select a coverage amount that covers your loved ones for the number of years that you expect them to rely on your income.

Every parent should consider having life insurance. While you may have an existing life insurance policy through your employer, it may not be enough once you become a new parent. Life insurance gives parents peace of mind in knowing that their children will be provided for no matter what. As you expand your household, you may take on large debts, such as a mortgage or a new car. New parents should think of life insurance as far more than an optional financial product. Life insurance is an essential part of planning for the future. It’s there to help protect your family in the long run, no matter what happens tomorrow or down the road.

/new-parents-highlight01_2x_1_vh9phc.png)

If you’re a stay-at-home parent, you should also consider taking on a life insurance policy. Why? Think of all the value you provide to your family as a stay-at-home parent. Replacing childcare alone would cost upwards of $16,000 per year—add on a housekeeper and it’s easy to see how a surviving parent would be left seriously struggling. In fact, if a stay-at-home parent made an annual salary, it would amount to about $162,000, according to Salary.com.

All of those costs add up and can be especially daunting during a stressful time when the family is trying to get back on their feet. So don't underestimate your value as a stay-at-home parent. Having a life insurance policy is another way to bridge the financial gap when your family needs it.

A beneficiary is the person, persons, or designated trust that receives your life insurance policy proceeds if you die while your policy is in force. As the policy owner, you designate your primary beneficiary (or beneficiaries) when you fill out your application.

For many parents, the primary beneficiary is usually your spouse, your life partner, or your children. Once you choose a life insurance policy that best suits your family’s needs, you’ll have peace of mind knowing that you’ve taken a tremendous step to protect your family's financial future. Life insurance will be there to help replace income, pay off debt, cover education costs, and alleviate living expenses that may pop up for your family, for years to come.

Every family is different. That matters when it comes to choosing the best life insurance policy for your family’s needs. There are two basic types of life insurance: whole and term.

Whole life insurance is permanent and stays in effect, as long as the premium is paid, typically for the entire life of the insured. Term life insurance provides life insurance coverage for a specific period of time. At Ethos, we offer term lengths between 10 and 30 years and coverage options from $20,000 to $1.5 million, With the term life insurance available with Ethos, you will pay a fixed premium for the duration of the policy, meaning your rate will never increase during your initial term.

How do you choose the best plan for your family’s needs? First, consider your current financial situation. For example, if you're a brand new parent you might want a 30-year term life policy that provides coverage until your child reaches adulthood. If your kids are in college, you might only need a 10-year term to cover educational expenses and any other unexpected plans in case you pass before they finish school.

As a new parent, a term life insurance policy may be the best option. Term life insurance can be up to 20X more affordable than a whole life policy. Plus, term life insurance provides coverage during the years you need it most and doesn't cost you money when you no longer need it. Of course, the best life insurance policy is the one that fits best with your situation and family needs. The premium rate that you pay could vary between the company and a variety of personal factors, such as age, health, and the amount of coverage you buy.

The goal of purchasing life insurance isn’t just to replace your earnings, but protect your loved ones from financial crises. Think of all the significant financial obligations that may be left behind if you died unexpectedly—from your home and business to debts that you’ve cosigned on.

A simple rule of thumb is to multiply your salary by 10 to replace lost income. Then, you’ll want to add on any debt you might have, including mortgage payments, estimated education costs, child and general household care, and other daily expenses. You may also want to add extra coverage that would help cover your spouse's income for a year or two, so that the surviving parent wouldn't have to worry about returning to work immediately while grieving. If your spouse is a stay-at-home parent, consider adding a rough estimate of what their annual salary would be if they suddenly had to return to work. Learn more about choosing the right type of life insurance plan and how much a life insurance policy will cost to protect your family.

You can use this life insurance calculator from Ethos to help get an estimate of how much coverage you need and what your policy could cost.

/new-parent-inset_2x_hhrukc.png)