How-to Guide for Handling Life Insurance Sales Challenges

Who doesn’t love an easy sale? But sometimes it’s those hard sales that make being an agent so rewarding. Here we’ll explore the four types of objections, the porcupine technique, and some examples with talking points to help you close sales (even the hard ones).

Clients have their own interests, concerns, and challenges, and those individualities make each objection unique in how the client feels and responds to you. Yet all objections, even with those nuances, will fall into one of four categories: misunderstanding, skepticism, drawback, and indifference. Here we explore each type.

The client misunderstands the solution.

Misunderstanding is when a potential client doesn’t understand something about your solution or is misinformed about your solutions by a competitor, friend, or advertisement. For example, they might say,

“I saw an ad on TV that said you only offer term life insurance, and I’m interested in whole life insurance.”

How to respond

Ask the client why those features or benefits are important to them. This gives you a chance to understand the reasoning behind their needs.

If they say it’s important for them to have life insurance for their entire life, you can say,

“I work with many clients to help them find the right life insurance policy for their needs, including whole life insurance. Here, let me show you.”

The client is skeptical of the company.

Skepticism is one of the best types of objections because it shows that buyers are interested enough that they’re looking for proof as to why they should purchase your solution. For example, they might ask,

“How do I know the company is reputable?”

How to respond

Empathize with the challenges the potential client faces, and then offer a source of proof. You can say,

“I understand your desire to work with a trustworthy and reputable life insurance provider, and I’d like to share a success story about another customer who felt just like you and is pleased with how Ethos has benefited them.”

The client is hung up on a drawback.

There are some things about your company or solutions that you simply can’t change. Think: features or capabilities. And while it’s clear that no solution will check all the boxes for every client, it’s still tough to accept when a potential client gets hung up on a drawback. So they might say,

”I don’t have time to go through the whole process of getting qualified for life insurance. I’ve heard it’s really complicated and takes a lot of work.”

How to respond

Reframe the drawback for the client. You can do this by minimizing the drawback and refocusing their attention on the positive aspects you’ve already discussed. So you might say,

“We’ve discussed how Ethos’ application takes less than 10 minutes to complete, and doesn’t require medical exams, just a few health questions, and almost always gives a same-day coverage offer (all while maintaining competitive pricing). Do those benefits outweigh similar offers you’ve received from other companies?”

The client is indifferent.

Indifference happens when the client doesn’t see a need for your offering or if they are happy with their current solution. For example,

“I don’t see the need for life insurance. If I die, my family will get the house and my baseball card collection.”

How to respond

The strategy here is to help the person see the gaps in their current method/thinking/situation, and offer help, such as,

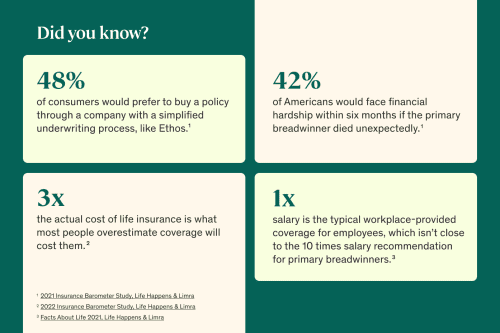

“Did you know that it’s recommended that primary breadwinners have 10 times their income in life insurance? Relying on your [baseball collection] may seem like a great idea, but it’s actually a risky, short-term solution.

The value of material possessions isn’t guaranteed, unlike the payout from a life insurance policy. With life insurance, you can help to ensure that your family has what they need to say in their home, send the kids to college, and more, creating a long-term support system.”

How to use the porcupine technique

One of the quickest ways to lose a sale is to lose control of the conversation. If you find yourself in a client-controlled situation, salespeople in all industries like to use the porcupine technique.

Think of it this way: If someone threw you a porcupine, what would you do? You’d likely throw that prickly creature right back to them.

You can use that same technique to take control of your client conversations. If they’re hitting you with rapid-fire questions, regain control of the conversation by answering their question with a question.

Often clients ask a yes or no question, which can stall a conversation, so throw that porcupine back at them and guide the conversation in the direction that can help secure the sale.

The porcupine technique in action

Do you offer a satisfaction guarantee?

If the insurance company offered a satisfaction guarantee, would it help you feel more comfortable getting started today?

Do I have to do a medical exam?

If you didn’t have to do a medical exam, would you be open to completing a 10-minute application today?

How much life insurance can I get for around $50 per month?

If we can find coverage for you today for around $50 per month, who would you like your beneficiary to be?

How you speak to clients is just as important as what you speak to them about. There are two things you’re trying to achieve when setting the foundation of the conversation: qualifying and building value.

Qualifying

This is your getting-to-know-you portion of the conversation. You want to uncover their pain points and what matters to them. Use questions like:

- What’s important to you in life?

- What are your goals in life?

- What do your future needs look like?

- What’s your current financial situation?

Building value

Using the information you’ve gathered from the qualifying questions, you can start to match solutions that speak to their pain points and goals/values. Use statements like:

- Here’s how you can protect those important things.

- Here’s how you can achieve those goals.

- Here’s how you can provide for those future needs.

- Here’s how this will complement your financial situation.

These strategies will help build rapport with the client, and they can also help mitigate or soften the objections that may come up later in your conversation.